On excessive pricing in the pharmaceuticals sector.

Recent EU and UK public enforcement decisions have put the pharmaceutical sector on notice for excessive pricing enforcement. From these decisions it is clear that, regarding long off-patent drugs, dominant undertakings should beware of setting prices at levels that significantly exceed reasonable profitability-based benchmarks, and that large [and opportunistic] price increases that are not associated with increases in costs, innovations or product improvements will not be tolerated.

According to EU and UK competition law, abuse of a dominant position can be divided into categories of exclusionary abuse and exploitative abuse. While the former category refers to the conduct that is aimed at excluding or weakening present competitors or potential entrants, the latter refers to a "purer" abuse directed at consumers or customers in the form of excessive prices. Although the enforcement has predominantly been on exclusionary abuses, recently there has been a surge of EU and the UK enforcement decisions based [primarily] on exploitative conduct in the pharmaceutical sector. Some of the notable decisions that we will discuss here are:

- Leadiant Biosciences was fined for excessive pricing in Spain, Italy and the Netherlands [ "Leadiant" ],1

- Advanz Pharma was fined for excessive pricing in the UK [ "Liothyronine" ],2

- Auden / Actavis was fined for excessive pricing in the UK [ "Hydrocortisone" ],3

- The European Commission ["EC"] accepted commitments by Aspen in relation to the excessive pricing of multiple drugs [ "Aspen" ].4

These cases are all centred around drugs that have been off-patent for decades, and have experienced dramatic price increases, without any notable product improvements that could potentially legitimise such price increases.

These cases are all centred around drugs that have been off-patent for decades, and have experienced dramatic price increases, without any notable product improvements that could potentially legitimise such price increases. In addition, these cases involve:

- gaining an orphan designation for market exclusivity [high barriers to entry], in the case of Leadiant and Hydrocortisone, and

- strategic de-branding of branded drugs to escape from regulatory or health agency oversight, in the case of Liothyronine and Hydrocortisone.

In this paper, we will analyse the aforementioned decisions through an economist's lens and contrast the approaches employed by the EC and the national competition authorities.

The overall structure of this Insight will be as follows. We will begin by providing some implications of the recent decisions for dominant undertakings, and discuss the possibility of (follow-on) damage claims in light of these decisions. After that we will discuss the influential United Brands standard. Finally, we will provide a detailed analysis of the recent decisions with respect to market definition, and the employed methodologies in relation to the United Brands standard.

Implications of the Recent Decisions

The recent decisions employ robust cost-plus and investor return methodologies. Although there are differences in the finer details of the analysis, there seems to be an overall consensus that the economic value (and hence the price) of long off-patent drugs should not be significantly different from their price benchmark, based on a reasonable return and/or profit.

Accordingly, these decisions suggest that dominant undertakings with off-patent drugs, should:

a) be able to justify [large] price increases in relation to costs,

b) consider that being outside of regulatory oversight or being in an

exclusivity regime does not give free rein to pricing decisions,

c) consider if their products give a reasonable return or profit.

Below, we will elaborate on some of the challenges these responsibilities may bring upon dominant undertakings and some of the associated uncertainties.

First, the decisions could be read to suggest that whenever a dominant undertaking becomes significantly more efficient, it may need to reduce its price based on its decreased product costs.

Second, it seems that the undertakings need to keep an eye on the industry dynamics and the overall profitability of comparable drugs to get a sense of what reasonable profit/return would entail.

Third, it may be desirable for dominant undertakings to have a good grasp of the intricate risks involved within a sector, such as risks that may be associated with the emergence of a superior medicine or the possibility of a failure of a project. This assessment of the risk is important when calculating the company’s WACC, and when assessing the IRR of a specific project. Firms that misestimate inherent risks may calculate improper reasonable return benchmarks and may either end-up making less than reasonable return/profit or in contrast they may make excessive profits that could take the attention of competition authorities.

Fourth, the case-law does not yet make it clear what the lower boundary is at which prices become excessive. Even if one abstracts from the unfairness limb, non-cost factors and other comparators, the excessiveness limb does not provide a precise formula. The profitability benchmarks that are used in the excessiveness limb may diverge from each other, and it is not immediately clear what magnitude of deviation from the reasonable benchmark can be considered excessive.

Considering the decisions discussed in this Insight, the lowest measure of excessiveness is found in Leadiant in Italy. The Italian authority found that the price was excessive when it was 60%-100% above the cost-plus benchmark price, suggesting that a reasonable threshold lies somewhere below a price that is 1.6 times higher than the cost-plus benchmark price.

Furthermore, it is useful to note that relatively recent judgment of AKKA / LAA indicated that only prices that are “significantly and persistently” excessive can amount to be an abuse and that in some of the aforementioned decisions, the authorities based their excessiveness assessments on the prices or margins/returns being “significantly” higher than respective reasonable benchmarks.5

In Aspen, the European commission used this terminology and attempted to clarify what significant deviation from a given benchmark could mean. The EC, while accepting that what significant entails may be context-specific, seemed to suggest a distributional approach to detect significant deviations. In assessing the magnitude of excessiveness of the prices, it considered the distribution of comparator products’ margins and noted that the EBITDA margins of the undertaking lay significantly above the 90-percentile of comparators, whereas gross margins were slightly higher than the respective 90-percentile.6 This implies that the price is only considered excessive if the resulting margin is significantly above that of the highest comparator margin. It remains to be seen whether the case-law provides more clarity on a threshold point for excessiveness and whether the distributional approach would be widely embraced.

Fifth, in Liothyronine and Hydrocortisone, the CMA rejected the use of a portfolio pricing approach citing the CAT judgment of Napp. However, economic theory suggests that a portfolio pricing approach might be relevant in some cases where certain cost related decisions concern multiple products and firms face real uncertainties about the success rate of its individual products. It remains to be seen how the authorities and the courts of the EU would approach to the portfolio pricing approach - would they outright the reject the approach or would they embrace it in some situations?

Damages Litigation

The aforementioned public enforcement decisions punish or correct abusive conduct of dominant undertakings and try to deter such behaviour from happening in the future. These decisions also open up the possibility for follow-on and stand-alone claims on behalf of damaged parties. Parties who might have been damaged as a result of the aforementioned conduct, except for the conduct in Aspen as this was a commitment decision, may claim compensation, without having to prove the existence of an infringement.

Depending on the national healthcare system, the excessive pricing conduct might have resulted in damages with national healthcare agencies, private or public healthcare insurers, hospitals, pharmacies, taxpayers, or the patients / consumers themselves.

Potential claims would be based on a counterfactual price to estimate the damages incurred. To arrive at a counterfactual price, the particulars of the case need to considered and various benchmarks can be taken into account. Potential counterfactual prices, among other things, could be:

a) A historical non-abusive price point, potentially corrected for cost increases.

b) The price of a comparable product.

c) The [average] price resulting from the cost-plus analysis in the infringement decision.

d) Prices of the same product in another geographical market.

The courts may decide on a single benchmark as the counterfactual price or take the average (or maximum) of various viable benchmarks. Alternatively, the court could add a small but significant differential on the used benchmark.

Another important factor to consider is the extent of pass-on. Depending on the health care system in which the infringement occurred, the excessive price may have been paid by different institutions But, if those institutions have then recovered their costs by increasing premia, increasing patient contributions, applying for extra government funding, etc., the damages could have been fully or partially passed-on to other actors in the health care system.

These decisions also open up the possibility for follow-on and stand-alone claims on behalf of damaged parties.

United Brands Standard

The influential United Brands standard on excessive pricing has given shape to the recent enforcement decisions in various ways. In United Brands, the ECJ ruled that if a dominant undertaking reaps benefits that result from its dominant position and charges excessive prices that bear no reasonable relation to the economic value of the product, then it would constitute an abuse.7 This implies that dominant undertakings need to act against their short-run (rational) instincts of reaping benefits and, to some extent, self-regulate, i.e. set prices as-if there was "normal and sufficiently effective" competition.8

United Brands also sets forward an influential two-stage criterion to determine whether prices constitute an exploitative abuse.9 The two-stage criterion is cumulative and consists of an excessiveness limb and an unfairness limb. While the first stage [excessiveness limb] evaluates whether prices are excessive in relation to costs, the second stage [unfairness limb] considers whether prices are unfair in themselves or in comparison to competing products.

The recent enforcement decisions on excessive pricing use methods based on the United Brands two-stage criterion, albeit with different cost-excess methodologies [excessiveness limb] and varying interpretations of the relevance of comparator benchmarks [unfairness limb].

In our analysis, we will describe the methodologies the authorities employed in relation to each of the two limbs. However, this does not mean that certain facts or analysis cannot be relevant for both limbs at the same time. For example, excessiveness can be investigated using the reasonable return for comparable products, while [un]fairness of prices can be assessed considering the additional innovativeness which could be also relevant for the cost-plus calculation.

Before analysing the decisions in detail, it is useful to briefly explain the approaches that the authorities used in determining the existence of market dominance.

Market Definition and Dominance

In all aforementioned cases, the national authorities and the EC employed narrow market definitions. Markets were defined on the national level, and constituted only the molecular substance, or even narrower, only the specific production method of the molecular substance. Dominance of the respective undertakings was determined by mainly relying upon the very high market shares (>60%) on the respective markets.10

It is important to note that the authorities based their narrow market definitions on the observation that other competitor drugs or competitor products manufactured by alternative methods did not constitute significant competitive constraints even though some of these competitor drugs might have been, to some extent, therapeutic substitutes.11

Furthermore, some authorities cited additional factors such as market exclusivity, exclusivity agreements with suppliers, and the lack of countervailing buyer power to have contributed to the dominant position of the undertakings.12

The recent enforcement decisions on excessive pricing use methods based on the United Brands two-stage criterion, albeit with different cost-excess methodologies [excessiveness limb] and varying interpretations of the relevance of comparator benchmarks [unfairness limb].

Excessivness Limb

Through the excessiveness limb of the United Brands standard, competition authorities attempt to assess whether the profits or returns of a firm are excessive compared to the costs and expenses related to the product.

In effective competition, firms may be expected to earn a reasonable level of profit or return on their costs or investments. Without such profits, firms may not enter the market, or may not make the necessary investments to continue or improve production. In a market where one firm is dominant, the firm may leverage its market power to earn above-reasonable or excessive profits, by charging excessive prices.

The threshold of what level of profits (and prices) can still be considered reasonable is context dependent and there are multiple ways to measure profitability. In any event, an economically sound profitability measure would consider direct and indirect costs that can be associated with the production of the product and should take into account the inherent risks and opportunity costs of such activity and industry-specific intricacies.

In the context of excessive pricing, competition authorities can use various methods to assess the profitability of firms, and the excessiveness of their prices. These methods can be divided into two categories:

- Cost-Plus: Authorities calculate a cost-plus benchmark price for the product, which can be derived from adding a reasonable gross margin, return on sales [ROS] or a reasonable return on capital employed [ROCE] multiplied with an appropriate capital base measure to the [per-unit] cost. This benchmark is then compared to the realised price. The authority will then determine if the realised price is unreasonably or excessively above the benchmark,

- Reasonable Return: Authorities will investigate what level of internal rate of return (IRR) is

to serve as a reasonable benchmark. This benchmark is then compared to the IRR realised on the cash-flow of the product-project. The authority will then determine whether the realised IRR is unreasonable or excessively above the benchmark, from the viewpoint of an [ex-ante] investor.

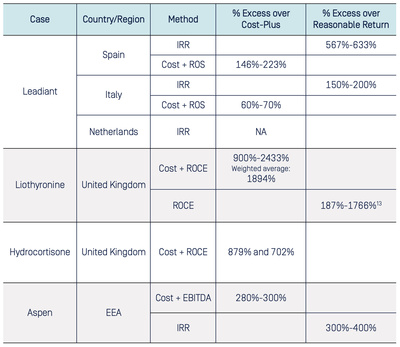

In the following subsections, we will explain what approaches the authorities used in relation to this limb in the cases at hand. In Table 4–1 below we summarise the findings of the different decisions. It is apparent from the table that most decisions employ more than one method to determine the excessiveness of the prices or profits.

The estimation results are typically a range of values. This stems from the fact that either the relevant price information is confidential, or from the fact that some authorities conducted multiple calculations with slight variations. Such variations are done to ensure the robustness of the estimate. The authority in question does not wish to estimate a precise figure but give a reliable indication that the prices and/or profits were indeed excessive.

The lowest degree of excessiveness found across the different cases is 60%-70% over the cost-plus benchmark price for Leadiant in Italy, while the highest degree is for Liothyronine in the United Kingdom with 2433% over the cost-plus benchmark price.

The percentages in the table are calculated as one would an overcharge in cartel damages, the percentage that the actual price or return is larger than the relevant benchmark. The 60%-70% excess of Leadiant in Italy should be interpreted as the realised prices being 60%-70% above the benchmark price. Put in other words, the Italian Leadiant prices are 1.6 to 1.7 times higher than the benchmark price.

Table 4-1. Price excessiveness methodologies and results.

Source: Respective decisions. Excess over cost-plus is calculated by dividing the excess by cost-plus. Excess over internal return is calculated by dividing the excess by the reasonable return.13

Leadiant

Leadiant is a case characterized by sharp price increases subsequent to or just before the firm attained an orphan designation and market exclusivity from the European Medicines Agency (“EMA”). The competition authorities of Spain [“the CNMC”] and Italy [“the AGCM”] employed both the cost-plus and IRR analysis method, while it appears that only latter method was used by the Dutch competition authority [“the ACM”]14. We start by explaining the common IRR analysis.

The CNMC, the AGCM and the ACM, each calculated the internal rate of return [IRR] that resulted from the orphan designation application. Specifically, the CNMC, the AGCM used the realised and expected cash flows in the market exclusivity period which ends at 2027.15 The authorities then compared the estimated IRR to the weighted average cost of capital [WACC]. In this context the WACC serves as the rate of reasonable return that investors would require to invest in the company.16 All authorities used a “conservative” WACC of 15%, and found that the project yielded excessive returns compared to this benchmark, indicating excessive prices.17 Specifically, the Italian authority noted that the IRR was at-least 150%-200% higher than the WACC, whereas the Spanish authority found that the IRR can be infinite and is 100%-110% according to the most conservative calculation, or 567%-633% above the benchmark.18

In general, the IRR analyses were conducted after most of the cash-flows were realized and the success of the project was already largely determined. Therefore, one could adjust the cost estimates or the WACC to realistically account for the project-specific ex-ante risks that investors might have faced.19 To this end, the ACM, in its IRR analysis, took into account the possibility that the orphan designation application would fail, when calculating the IRR of the project. However, the Spanish and Italian authorities considered that the of cost of capital already accounted for the low risks associated with the project.20

The AGCM and CNMC also conducted cost-plus analyses. Both authorities added a reasonable ROS to the costs associated with the product. The cost-base that the authorities considered, accounted for the costs that were directly related to the product, and indirect costs that were estimated by taking an appropriate percentage of shared costs that the undertaking incurred for its whole portfolio. The AGCM and CNM estimated the reasonable ROS benchmark by using the average operating margins of a comparable set of pharmaceutical companies in the EU in the relevant time period, which were given at 21% and 22%, respectively.21 Using these cost-bases and profitability benchmarks, the Spanish authority found that the cost-plus excess amounted to 146%- 223% [depending on the variation of the relevant period], whereas the Italian authority obtained an excess figures of 60%-70% and 90%-100%. As a result, both authorities find that Leadiant’s prices were excessive.22

Liothyronine and Hydrocortisone

The Competition & Markets Authority decision [“the CMA”] issued two almost simultaneous decisions in the cases Liothyronine and Hydrocortisone. Both cases involved the de-branding of drugs and sharp price increases. The CMA used the cost-plus method to assess the excessiveness of the prices. Since the approaches that the CMA employed in both cases are slightly differed, we will explain them separately.

In Liothyronine, the authority calculated the cost-plus benchmark price by using the relevant direct and indirect costs and a reasonable ROCE multiplied by the employed capital base of the company. The capital-base in this calculation consists of the product-attributable tangible and intangible assets, and working capital. The authority considered that a reasonable ROCE rate is a reasonable WACC of 10%. To obtain this estimate for the WACC, the authority used a reasonable cost of debt and a cost of equity that was calculated using the capital asset pricing model [CAPM] formula and an associated risk estimate which was derived from the average volatility of a set of comparable drugs.23 The resulting analysis of the CMA showed that the differential between the realized price and cost-plus price ranged between 900% and 2433% in the relevant period with a weighted average of 1894%, indicating excessive prices.24

Upon receiving objections from the parties, the CMA also conducted some sensitivity checks based on:

a) A higher cost of capital of 15% [excluding the working capital],

b) A larger capital-base to incorporate the possibility that the product may fail,

c) A different method of allocating shared costs.

These sensitivity checks increased the cost-plus price but still indicated an excess in the range of 321%-1985%.25

The CMA rejected the other adjustments put forward by the parties, such as the inclusion of a positive small company premium for the cost of capital estimation, incorporation of portfolio-pricing, and multi-firm approaches that would have increased the cost-plus price.26

In Hydrocortisone, the CMA calculated the cost-plus price by calculating the direct and indirect costs and adding a reasonable ROCE rate of 5-10%, multiplied by the relevant capital base of the undertaking. The CMA concluded that this ROCE rate was appropriate as it was equal to the WACC estimate that the undertaking used in its valuation of the company before acquiring it.27 The CMA calculated that the average excess for 10 mg tablets amounted to be 879% whereas the average excess for 20 mg tablets was 702%.28

The CMA also received some objections to its calculations. These objections were centred around the non-appropriateness of using a single-product cost-plus analysis, the non-appropriateness of using ROCE for an allegedly “asset-light” business, and the low [reasonable] rate of return on capital used in the cost-plus. The CMA rejected these adjustments.29

Aspen

The case of Aspen originates from the Italian competition authority decision in which it had fined Aspen for excessive pricing of several off-patent cancer drugs. The European Commission followed up to investigate the same infringement for the whole EEA, excluding Italy, and issued a commitment decision. The EC conducted a cost-plus analysis by adding a reasonable gross, and earnings before interest, taxes, depreciation, and amortization [EBITDA] margins to the relevant cost-base.30 The EC relied on the gross and EBITDA average margins of comparable products, which were 54% and 23% respectively.31 The EC found that the prices of Aspen’s drugs are 280-300% higher than the cost-plus price calculated with these margins, indicating that the prices of Aspen were excessive.32

In calculating the cost-base of Aspen, the EC did not take into account the acquiring costs that Aspen incurred when taking over the drugs from another firm. The EC justified this omission by noting the circularity problem that arises from this line of argument, as the acquiring price is [possibly] a function of expectations of future prices – which might have been anticompetitive.33

Nevertheless, the EC conducted a complementary IRR analysis while

taking into account the acquisition costs, and derived an IRR around

40%-50% which lies ‘well- above’ the ex-ante WACC estimate of Aspen which was given at 10%.34 According to the EC, these additional analyses confirmed its cost-plus assessment that the prices were excessive.

Broadly speaking, authorities can investigate whether there are factors that are not explicitly accounted for in the excessiveness limb, but that could justify a price higher than a reasonable profitability-based price benchmark.

Fairness Limb

We will now describe how the authorities implemented their methodology with respect to the unfairness limb. Broadly speaking, authorities can investigate whether there are factors that are not explicitly accounted for in the excessiveness limb, but that could justify a price higher than a reasonable profitability-based price benchmark. These could be, among other things, innovativeness of the product, improvements made to the product, and demand-related factors. The authorities can also check whether there are comparator benchmarks that would indicate that the economic value of the product is higher than the ‘cost-plus price’ or that actual prices are not too far from what could have been expected from effective competition.

The authorities in the aforementioned cases used relatively similar approaches in relation to this limb, mostly focusing on the “unfairness of itself,” relying upon the fact that the drugs had been off-patent for a long time, and that there were no associated innovations and/or product improvements. Nevertheless, the authorities also considered the suitability of various comparators, albeit to a varying extent. Especially the CMA gave detailed consideration to comparators put forward by the undertakings. This was done in the context of the Phenytoin judgement in the UK, which ruled that such comparators need to be taken into account even when the authority bases its conclusion on the unfairness in itself part of the limb.35

Leadiant

In Leadiant, the AGCM, the CNMC, and the ACM based their unfairness assessments mostly on the abnormal price increases that CDCA-Leadiant enjoyed following the orphan designation, while being effectively the same product as the long off-patent drug Xenbilox.36 The authorities concluded that the high prices were not associated with any increase in therapeutic value, any significant improvement in efficiency, or safety of the drug.37 Furthermore, the undertaking did not conduct any innovative activity or research in relation to the product.38

The CNMC and AGCM also considered a variety of comparator benchmarks, including the prices of Leadiant in other EU countries and the prices of alternative drugs based on another substance, cholic acid, but concluded that these do not constitute useful comparators.39 Regarding the price levels in other EU countries, the authorities stated that these prices might have been inflated due to potentially abusive conduct of the undertaking in those countries.40 Regarding the price of other cholic acid drugs, the Spanish authority mainly alluded to the therapeutical advantages and [clinical] desirability of CDCA-Leadiant over these comparators, while the Italian authority pointed out that the cholic acid-based drugs likely enjoyed a significant markup due to their orphan status/market exclusivity and were therefore unsuitable as a comparator.41 The Dutch competition authority considered the cost of magistral production as a viable comparator, and stated that the prices of Leadiant were significantly higher than those costs, indicating again the unfairness of the prices.42

Liothyronine and Hydrocortisone

In the Liothyronine and Hydrocortisone decisions, the CMA employed largely similar approaches to show the unfairness of the prices of respective drugs, mainly based on “unfairness in itself” analysis. In both decisions, the CMA referred to the discrepancy between the realized prices and the economic value of the drugs. The CMA stated that normally, prices of drugs that are in the third phase of their life cycle, would bear no relation to their therapeutic value. Instead, their prices are determined by the level of competition, and consequently their price should be reasonably close to the cost-plus price benchmark. According to the CMA, the market power of the undertakings and other features of the respective markets (including – high barriers to entry, the lack of countervailing buyer power and regularity constraints), allowed the undertakings to charge prices beyond the economic value of the products.

Furthermore, the CMA stated that significant price increases observed in both cases were not associated with innovations, increasing production costs, or other demand factors that would have increased the economic value of the product beyond its cost-plus price benchmark.43 In each case, the authority considered a variety of factors and comparators that could be relevant for the economic value and fairness of the product, and we will discuss these separately.

In Liothyronine, the CMA stated two additional arguments that might indicate the non-existence of demand-side factors which could have increased the economic value of the product.44 Firstly, the authority considered that the buyers were not willing to pay a premium for the product. Secondly, the product did not have a higher therapeutic and economic value than the comparator drug Levothyroxine, which was priced significantly lower. According to the CMA, the fact that this comparator was generally preferred over Liothyronine, and that the former’s price was lower than the cost-plus price of Liothyronine, indicated that there was no reason to add an additional premium on the cost-plus price of Liothyronine.45

Furthermore, the CMA, following the precedent of Phenytoin, assessed the viability of various comparators that were put forward by the dominant undertaking that could be relevant for the product’s economic value, namely: 46

a) Post entry prices: Prices that were realized after entry into the market had occurred.

b) Forecast prices: Future expectations of the undertaking and two competitors on prices after entry.

c) Entry incentivizing prices: Pre-entry prices that were alleged to incentivize entry.

d) Cournot modelling prices: Equilibrium price estimations using a quantity competition model.

e) Multi-firm prices: Cost-plus prices derived by applying a multi-firm per-unit fixed cost.

The CMA rejected the validity of all these benchmarks. In relation to the first three benchmarks, the authority concluded that prices cannot escape competition law just because they are followed by entry, and that post-entry and forecast prices might not constitute reliable benchmarks as these prices are likely to be contaminated by the pre-entry prices that might have been excessive in the first place. The CMA also iterated that the prevailing post-entry prices did not reach the effective competitive levels that would have been expected from a mature market of generic drugs.47

In relation to the Cournot modelling benchmark, the CMA rejected that the modelling assumptions, including quantity competition, were appropriate for the case at hand. Furthermore, the authority considered that the use of a multi-firm price benchmark is not sensible, as according to such a benchmark the price would be increasing with respect to the entry costs and the number of active firms in the market, and this would “defeat the purpose of the law”.48

In Hydrocortisone, the CMA considered two additional benchmarks, (i) the [then] current prices of the competing hydrocortisone tables and (ii) the erosion of the dominant undertaking’s prices. As to (i), the authority considered that these prices constitute a good benchmark for what consumers are willing to pay for those tablets in normal competition, and the fact that they lie below the cost-plus price of Hydrocortisone indicates that the economic value of the drug is likely not higher than its cost-plus price. As to (ii), the authority stated that the fact that prices were eroding was an indication that prices in the infringement period were significantly higher than the product’s economic value.49

Aspen

In Aspen, the EC based its conclusion on the prices being “unfair in themselves”, while rejecting the suitability of various potential comparator benchmarks. The EC considered potential risk-taking activity and innovations conducted by Aspen and noted the off-patent status of the drugs. According to the EC, the undertaking did not conduct additional innovations and the costs of earlier innovations and risk-taking activities may be deemed to have already been recouped in the patent period.50 Furthermore, it noted the sharp price increases in comparison to the limited increases in the cost-base.51

Accordingly, in its assessment, the EC concluded that the prices of Aspen were unfair in themselves.52

Any opinions expressed in this communication are personal and not attributable to the Competition Economists Group

[1] CNMC decision of 14 November 2022, case S/0028/20, Leadiant: https://www.cnmc.es/sites/defa... [“Leadiant decision - Spain”]

AGCM decision of 31 May 2022: https://en.agcm.it/dotcmsdoc/p...; [English], [“Leadiant decision - Italy”]

ACM decision of 1 July 2021, case ACM/UIT/554938: https://www.acm.nl/sites/defau... [English Summary], [“First Leadiant decision [summary] - the Netherlands”],

ACM decision of 22 June 2023, case ACM/UIT/590746: https://www.acm.nl/system/file... [English- Summary- On Objections] [“Second Leadiant decision [summary] - the Netherlands”]

[2] CMA decision of 29 July 2021, case CE-50395, Liothyronine tablets: https://assets.publishing.service.gov.uk/media/61b8755de90e07043f2b98ff/Case_50395_-_Decision_final___.pdf [“Liothyronine decision”]

[3] CMA decision of 15 July 2021, case CE-50277, Hydrocortisone tablets: https://assets.publishing.service.gov.uk/media/624597bbe90e075f0b5a3da4/Case_50277_Decision.pdf [“Hydrocortisone decision”]

[4] Commission decision 10 Feb 2021, case AT.40394, Aspen: https://ec.europa.eu/competition/antitrust/cases/dec_docs/40394/40394_5350_5.pdf [“Aspen decision”]

[5] EU Court of Justice judgment of 14 September 2017, Case C- 177/16, AKKA/LAA v the Latvian Competition Council, paras. 55-56.

[6] Aspen decision, para. 184, fn. 125.

[7] European Court of Justice judgment of 14 Feb 1978, case 27/76, United Brands v Commission. ["United Brands"]. paras. 249-250.

[8]

This interpretation is in some contrast with the AEC principle

that condemns [exclusionary] abusive conduct that cannot be reconciled

with short-run rational behaviour. See United Brands, para. 249.

[9] United Brands, para. 252.

[10]

Some of the drugs considered in Aspen did have less than 50%

market share in some national markets for a period of time. See Aspen decision, fns. 43-44. Furthermore, in Hydrocortisone,

relevant Hydrocortisone tablets had market shares exceeding 60% after

entry in a certain interval of the infringement period. See Hydrocortisone decision, para. 4.230. In Leadiant and Liothyronine

cases, the undertakings had 100% market share in the considered infringement periods.

[11] See Aspen decision, paras. 27-34.

[12] See Aspen

decision, paras. 65 and 70-72, for example.

[13] Liothyronine

decision, para. 5.190 - Table 5.6.

[14]

From the ACM decision, it appears that the ACM used the IRR

method. It states on para.12 of the English summary of the original

decision: ‘Leadiant’s internal rate of return on the project was

extremely high, even on the basis of conservative assumptions. In its

assessment, ACM took account of a required rate of return of 15%

(reasonable return for investors)’. However, the details regarding

these calculations are not publicly available. In this Insights, we

assume that they employed that method.

[15]

The internal rate of returns was calculated in regular an in

incremental fashion by the AGCM and the CNMC assuming that prior-orphan

designation prices would stay the same at the same level in case of

failure of the application. First Leadiant decision [summary] -

the Netherlands, para. 12. See Leadiant decision - Spain, para. 554 and

Leadiant decision - Italy, para. 511-514.

[16]

Estimates of WACC can be derived using the capital assets pricing

model [CAPM], by calculating the relative volatility of the firm’s

equity and the cost of its debt or can be inferred by making use of WACC

figures of comparable products.

[17] First Leadiant decision [summary] - the Netherlands, para. 12. Leadiant decision - Italy, paras. 513-514. Leadiant decision - Spain, para. 545. The Italian authority also considered a less conservative WACC of 12%.

[18] Leadiant decision - Spain, para. 556. Leadiant decision - Italy, para. 514.

[19]

Similarly, if the undertakings had conducted ex-ante calculations

before making investment decisions, the relevant information can be used

to assess the real risks that the undertakings had faced.

[20]

The AGCM and the CNMC also attached importance to the ex-ante

risk-return analyses conducted by the undertaking before the

infringement period, while dismissing the submitted risk analyses that

were only conducted ex-post. Original Leadiant decision [summary] - the Netherlands, para. 11.

[21] Leadiant decision - Spain, para. 466-467. Leadiant decision - Italy, para. 267.

[22] Leadiant decision - Spain, para. 475. Leadiant decision

- Italy, para. 268. The difference can be attributable to the fact that

in Italy the responsible negotiating committee was able to reduce the

prices of Leadiant substantially within the infringement period.

[23]

According to the CAPM theory, an efficient stocks’ return can be

derived using its beta / volatility coefficient which is given by the

ratio between its covariance with a market (indicator) portfolio and

risk and the variance of the market portfolio. See also Annex 4 of Liothyronine decision.

[24] Liothyronine decision, paras. 5.184-5.186.

[25] Liothyronine decision, para. 5.187, table 5.5.

[26] CMA’s counter arguments on these points can be found in paras, paras. 4.129, 5.197, and 5.195.

[27] Hydrocortisone decision, paras. 5.201- 5.205.

[28] Hydrocortisone decision, para. 5.225.

[29] Hydrocortisone decision, paras. 5.268-5.291.

[30]

In its assessment, the EC did not make use of EBIT margins as

there had been some significant impairments in the tangible asset

accounts in the considered period making EBIT margins possibly less

reliable. See Aspen decision, paras. 119-121.

[31] Aspen decision, para. 131.

[32] Aspen decision, para. 140 and table 4.

[33] Aspen decision, para. 156.

[34] Aspen decision, para. 158 and fn.110.

[35]

UK Court of Appeal judgment of 10 March 2020, Case No:

C3/2018/1847 & 1874. Flynn Pharma Ltd & Anr v CMA Phenytoin,

paras. 97,116 and 270. Available at: https://www.catribunal.org.uk/sites/cat/files/2020-04/1275-76_Flynn_CoA_Judgment_100320.pdf

[36] Leadiant decision- Spain, para. 569-570. Leadiant decision- Italy, para. 559, 573-574. First Leadiant decision- the Netherlands, para. 13.

[37] Leadiant decision-Spain, para. 573. Leadiant decision - Italy, para. 559. First Leadiant decision- the Netherlands, para. 13.

[38]

The Spanish and the Italian authorities argued also that it is not

possible or useful to directly calculate the price or the therapeutic

value of the drug based on willingness to pay of buyers since the drug

is vital for the patients and their willingness to pay can be assumed to

be unbounded. See Leadiant decision-Spain, para. 441. Leadiant decision-Italy, para. 559.

[39]

The Italian authority also considered two benchmark prices based on

the pricing of a set of 75 orphan drugs and a set of 14 orphan drugs.

The former set included unidentified drugs while the second consisted of

drugs that are supposedly prescribed for similar indications. The

Italian authority concluded that these comparators are unsuitable citing

factors such as the unaccounted demand differences and innovativeness

of some of drugs in the first comparator set. See Leadiant decision – Italy, paras. 539- 546.

[40] Leadiant decision - Spain, paras. 576-577. Leadiant decision - Italy, para. 552.

[41] Leadiant decision - Spain, para. 583. Leadiant decision-Italy, para. 547.

[42] First Leadiant decision- the Netherlands, para. 13.

[43] Liothyronine decision, para. 5.251. Hydrocortisone decision, para. 5.296.

[44] Liothyronine decision, para. 5.208.

[45] Liothyronine

decision, para. 5.223. It is useful to make two remarks. First, it is

our impression that while the authority argued on the one hand the

therapeutic drug of such a drug (a drug in its third phase) is largely

irrelevant for an excessiveness-unfairness analysis, it used the

therapeutic value of a similar drug to support its conclusion on the

unfairness of the prices. Second, the authority did not seem to attach

any importance to the possibility that the willingness to pay of the

limited set of users of Liothyronine can be significantly higher than their willingness to pay for the first-choice drug.

[46] Liothyronine decision, para. 5.281.

[47] Liothyronine decision, para. 5.285.

[48] Liothyronine decision, para. 5.357.

[49] Hydrocortisone decision, paras. 5.436-5.451, 5.433, 5.371-5.388.

[50] Aspen decision, paras. 169- 170, 165.

[51] Aspen decision, para. 165.

[52] Aspen decision, paras. 172-175.